This chapter deals with the main social protection programs for PWD in India. As noted in Chapter 7, this is an area where the commitments of the PWD Act are rather circumscribed. In practice, even the commitments of the Act on certain social protection schemes have not been met often. Nonetheless, a number of measures are either gradually improving or have potential for expansion, so are worth exploring.

There are many elements of the social protection system to which PWD and their households may be entitled not due to disability but due to poverty, social category or other indicators. These include most importantly the PDS food scheme for poor households. However, the focus of this chapter is on specific commitments and schemes that PWD are entitled to as a result of their disability (or disability plus some other indicator such as poverty). The main programs discussed are:

-

reservations under various centrally-sponsored anti-poverty programs which operate throughout rural areas of India, in particular public works, targeted credit and publicly-financed housing schemes for the poor

-

unemployment allowances for PWD

-

“social pensions” for destitute PWD, i.e. monthly social assistance cash benefits

-

different forms of insurance in cases of disability, including schemes for civil servants and the formal private sector, existing schemes for informal sector workers in some parts of the country, and proposals for expansion of social insurance to the unorganized sector

The social protection system specifically for PWD thus consists of both social welfare and social insurance interventions. However, for the vast majority, insurance-based schemes are not yet a reality. Overall, the public social protection system for PWD who are not in the formal sector is in design parsimonious on most states, and in practice offers low coverage and limited financial protection. Even in the formal sector, there are a range of issues in design and actuarial soundness of disability (and broader social) insurance systems for the public sector.

Poverty Alleviation and Social Assistance Schemes for PWD

• Reservations in anti-poverty programmes: The PWD Act commits governments to reservation of not less than 3 percent in all poverty alleviation schemes for the benefit of PWD. This section looks at recent performance on a few major schemes: public works under SGRY; subsidized credit for BPL households under SGSY; and the IAY housing program for the rural poor. While the Act is relatively clear on the 3 percent reservation, this has been interpreted in somewhat different ways in each scheme. For SGRY, there is mention of parents of CWD rather than adult PWD workers, on the assumption perhaps that PWD are not able to engage in work. However, while parents are mentioned as a target group, there is no specific quota target for their employment under the scheme (unlike other target groups like women and SC/ST for whom specific target shares are noted). For the new NREGS, there is no specific mention at all of PWD as a target group in the guidelines. In IAY, people with disabilities are mentioned as a priority target group (among several categories), but no specific quantitative target is set. In the case of SGSY, the guidelines are more specific, and require that 3 percent of beneficiaries annually be PWD.

• Reporting formats from poverty alleviation programs do not in all cases make it easy to know what share of beneficiaries are PWD. However, where data are clear, it appears that PWD are well below 3 percent of beneficiaries in all schemes. Data for SGSY are presented in Table 6.1 below, and indicate that the share of PWD beneficiaries has never been above 1 percent of total swarozgaris between 1999 and 2004. No single state in 2003-04 reported meeting the PWD quota, with AP the best performer at 2.1 percent of beneficiaries. Several large states with high poverty rates reported PWD shares below 0.5 percent of total SGSY beneficiaries (e.g. UP, West Bengal, Orissa, Jammu and Kashmir and Bihar). Equally, SGSY coverage rates in the five year period as a share of total adult PWD have been minimal, with 35,914 PWD beneficiaries accounting for around 0.3 percent of total working age PWD (15-59). Even excluding non-workers, the share of PWD assisted by SGSY in the period is only 0.7 percent of the working PWD population.

• As with other social groups, a challenge in mobilizing access to SGSY funds is formation and capacity building of SHGs among PWD. Without functioning PWD SHGs, revealed demand for the program will always remain low. Many states in their SGSY programs have started to use NGOs to mobilize SHG formation and build their capacity. It seems that such efforts need to include a specific disability focus as well if the SGSY is ever to approach its target levels of PWD beneficiary share. There are promising examples. In AP, efforts to support PWD SHGs under the Velugu program have resulted in formation of almost 15,000 PWD SHGs. While much remains to be done to strengthen capacity, the higher rates of PWD coverage in AP’s poverty alleviation programs suggest initial impacts, albeit with some way to go.

|

Table 6.1: Proportion of PWD beneficiaries under SGSY, 1999-2004

|

||||||

| Financial Progress | 1999- 2000 |

2000- 2001 |

2001- 2002 |

2002- 2003 |

2003- 2004 |

Total / Average 99-04 |

| Total Swarozgaris | 933,868 | 1,006,152 | 937,468 | 826,267 | 892,890 | 4,596,645 |

| PWD Swarozgaris | 8,529 | 6,737 | 6,059 | 6,118 | 8,471 | 35,914 |

| %PWD/total | 0.91 | 0.67 | 0.65 | 0.74 | 0.95 | 0.78 |

| Per capita Investment(Rs.) | 17,113 | 21,481 | 21,284 | 21,666 | 22,685 | 20,846 |

Source: Ministry of Rural Development

One of the factors driving the apparently poor PWD outcomes on public works appears to be very low awareness in PWD households of the reservation. In the UP and TN rural survey, fully 94 percent of households were not aware of the reservation on public works schemes, and only 0.1 percent of PWD themselves had participated in any public works.

While SGRY performance on employment of disabled people appears to be poor, the 2005 National Rural Employment Guarantee Act (NREGS) has dropped the reservation for disabled people, with no mention of preferences for people with disabilities in either the Act itself or the implementing guidelines. This appears to be clearly inconsistent with the PWD Act, and efforts are ongoing to seek adjustment of the NREGS guidelines. An interesting joint effort between the state Government and disability NGOs is underway in AP to identify additional categories of works which would be better suited to employment of different disability categories. A second significant innovation in AP is that households with a disabled member are entitled to 150 days of public works employment per year, rather than the 100 days for other households under the Act. This can apply to any household member.

Performance on the IAY housing program is also well below commitments of the PWD Act. Recent data are available for fewer years, but 2003-04 data indicate that only around 0.8 of all beneficiaries were PWD. Again, there was some range statewise, but – with the exception of Manipur – not state met its quota, with again AP being the best performer with 2.3 percent of beneficiaries as PWD. In contrast, UP and Jammu and Kashmir reported no PWD beneficiaries at all in 2003-04, and many states having PWD rates of 0.2 percent or lower of total beneficiaries (e.g. Bihar, West Bengal, Orissa and Karnataka). Data for the period 1998-2003 also indicate very low state shares of PWD to total IAY beneficiaries, estimated to be less than half of percent of all IAY beneficiaries in the period.

|

Table 6.2: States/UTs with unemployment allowance (Rs), 2004

|

|

| State | UA per month |

| AP | Rs. 75 |

| Haryana | Yes |

| Meghalaya | Rs. 50 |

| Punjab | Rs. 150 to 400 |

| Sikkim | Rs. 500 |

| Tamil Nadu | Rs. 200 to 300 |

| West Bengal | Yes |

| Andaman and Nicobar | Rs. 100 |

| Chandigarh | Rs. 150 to 400 |

| Daman and Diu | Yes |

| Mizoram | Rs. 100/month |

| Pondicherry | Rs. 400 and 500 |

Source: MOLE.

Household survey data from 2004/05 provides the first nationally representative insight into coverage of disability social pensions, as well as into the incidence of coverage across different wealth categories and social groups. The findings are shown in Table 6.3 and 6.4 below. Several points are worth noting:

-

while coverage of disability social pensions is low across the entire population (at 0.3 percent of households nationally), they cover quite significant shares of households who have a disabled member (nationally, around 14 percent of such households)

-

there is wide variation across states in coverage rates. Given that disability social pensions are state-funded entirely, this reflects largely state-specific priority given to the program. However, the interesting feature is that coverage rates do not vary systematically according to the poverty rate in states (note that cross-state disability rates in official statistics are not very

great). Thus some lagging states such as Orissa, MP and Rajasthan have good coverage rates, while some richer states such as TN and especially Gujarat have lower than average rates. -

while state-specific benefit levels varied at the time of the survey, the median benefits reported as received by households indicate that there appears to be fairly low leakage of funds in terms of reporting beneficiaries getting less than their cash entitlements.

Table 6.3: Coverage rates of disability pensions by total HH population and HH with PWD, 2004/05

| % of all HH receiving disability pension | Implied % of PWD receiving disability pension | Median annual benefits among HH receiving (Rs) | |

| Jammu and Kashmir | 0.2 | 6.7 | 3,600 |

| HP | 1.1 | 42.9 | 2,266 |

| Punjab | 0.3 | 17.2 | 1,560 |

| Uttaranchal | 0.2 | 8.7 | 250 |

| Haryana | 0.8 | 37.2 | 2,819 |

| Rajasthan | 0.5 | 20.0 | 2,400 |

| Uttar Pradesh | 0.3 | 14.4 | 1,531 |

| Bihar | 0.2 | 8.8 | 1,473 |

| West Bengal | 0.1 | 4.3 | 6,000 |

| Jharkhand | 0.2 | 12.0 | 1,200 |

| Orissa | 0.8 | 28.8 | 1,054 |

| Chattisgarh | 0.3 | 14.9 | 1,436 |

| MP | 0.5 | 21.4 | 1,681 |

| Gujarat | 0.0 | 0.0 | |

| Maharashtra | 0.1 | 6.2 | 1,713 |

| Maharashtra | 0.1 | 6.2 | 1,713 |

| Andhra Pradesh | 0.1 | 5.6 | 633 |

| Karnataka | 0.8 | 44.9 | 2,273 |

| Kerala | 0.6 | 22.2 | 966 |

| Tamil Nadu | 0.1 | 3.8 | 1,575 |

| All India | 0.3 | 14.1 | 1,781 |

While coverage of disability social pensions is quite impressive in a number of states, the distributional pattern of coverage across wealth and social groups is more neutral, indicating considerable spending on the non-poor. In addition, as the richest, Brahmin and OBC households receive notably higher benefits than the poor and SC/ST households, the incidence of actual benefit receipts reports by households indicates real challenges in targeting. While the poorest quintile of households receive somewhat higher share of total benefits than their share in population, this is also true for the richest quintile, but not for example for the second poorest quintile. Equally, both SC and ST households capture notably less of total benefits than their population share.

|

Table 6.4: Coverage of disability social pensions by wealth, location and social category, 2004/05

|

|||

| % of households receiving benefits from NDP | Median benefits among households (Rs annual) | Share of total benefits capture by group (%) | |

| Poorest | 0.4 | 1,713 | 25.5 |

| Q2 | 0.3 | 1,605 | 20.6 |

| Q3 | 0.3 | 17.2 | 1,560 |

| Q4 | 0.3 | 1,539 | 12.5 |

| Richest | 0.3 | 2,771 | 23.5 |

| Rural | 0.3 | 1,856 | 89.1 |

| Urban | 0.1 | 1,335 | 10.9 |

| Brahmin | 0.2 | 1,868 | 3.1 |

| OBC | 0.3 | 1,860 | 49.0 |

| SC | 0.3 | 1,615 | 21.6 |

| ST | 0.2 | 1,601 | 5.0 |

| Other | 0.2 | 1,827 | 21.2 |

| All India | 0.3 | 1,781 | 100 |

Source: Ajwad (2006), Bank staff estimates, based on NCAER national HD survey in 2004/05.

|

Awareness of disability certification and cash benefits, rural UP and TN, 2005

|

|

| Certification as a disabled person | |

| Not aware | 56.2% |

| Aware | 19.8% |

| Benefited | 20.7% |

| Denied | 3.3% |

| Regular cash benefit to destitute or unemployed PWD | |

| Not aware | 61.5% |

| Aware | 25.6% |

| Benefited | 9.0% |

| Denied | 3.9% |

|

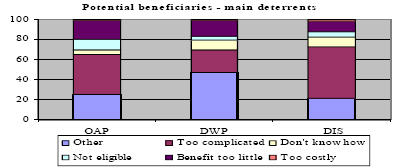

Figure 6.1: Main deterrents to application for social pensions by type of pension, Rajasthan, 2006

|

|

As seen in previous sections, the UP and TN survey explored knowledge of entitlements among PWD. To access the disability social pension or unemployment allowance, it is necessary first to have a disability card. In the survey, only 15 percent of PWD with moderate disability had such a card and around 21 percent of those with severe disabilities. Shortcomings in the identification and certification system are therefore to some extent driving relatively low coverage in the social protection system. However, and only 9 percent of them having benefited (Table 6.5). While awareness is not as low as several other PWD entitlements, lack of awareness is clearly an issue.

Disability Insurance in India

|

Table 6.6: Contributions and benefit targets for mandated disability insurance in India

|

|||

| Employees Pension Scheme |

8.33% that also covers old age and survivor benefit | 1 month | Replacement rate |

| Civil service pension Scheme |

None, financed from budget directly | Immediate | 1.52% X years of service X final 10 months wage with minimum 1310 rupees per month |

| Military pension Scheme |

None, financed from budget directly | immediate | Basic retirement pension plus 20% depending on rank |

|

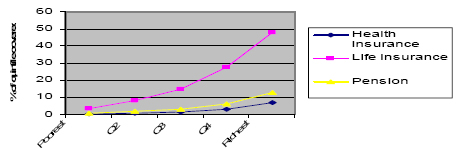

Figure 6.2: Coverage of health, life and pension insurance, 2004

|

|

In India, there is a large disparity in disability inflow rates between the rates reported for workers in the unexempted funds (which make contributions directly to EPFO and EPS) and those in the exempt funds (which operate in large establishments and opt out of the EPFO). In the case of civil servants, the financing comes directly from the budget. No reserves are set aside, just as in the case of old age pensions. This is starting to change however, as a new defined contribution scheme is being phased in for new civil service hires. In the case of the Employees’ Pension Scheme (EPS), the benefit is financed out of a common fund and contributions are pooled for old age and disability. Recent actuarial reports have identified an unfunded liability in the EPS signaling sustainability problems. In both cases, the premium required specifically for disability insurance coverage has not been calculated or separated. This is not surprising given that in neither EPS or the EPFO are the contributions (or lack thereof) set so as to generate long term actuarial balance. The new DC scheme that covers newly hired civil servants makes it necessary to rethink the simple - if opaque - financing arrangement for disability insurance that has operated so far.

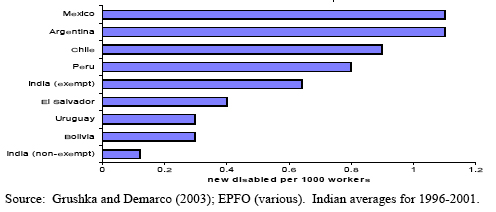

Reported disability inflow rates in India’s EPFO/EPS scheme are shown in Figure 6.3 below, and compared to rates in seven Latin American countries. Notably, the unexempted fund rates are the lowest in the table and nine times lower than those in the exempt funds. The reason for this low rate is not clear especially because the rate of actual disability is likely to be higher among the unexempted workers given that they have lower average wages than the exempted fund workers. Among the possible explanations is the fact that exempt funds can process claims “in-house” without having to approach the EPFO bureaucracy, and may therefore be more efficient in processing claims. The differentials – both in comparison to exempt funds and the other countries shown – raise questions on the efficiency of current social insurance

|

Figure 6.3: Disability inflow rates for contributory pension members in India and selected Latin American Countries, 2000-2002

|

|

Easily the largest scheme for unorganized sector workers is the Janashree Bima Yogana (JBY), which is a bundled life and total/partial permanent disability product provided by Life Insurance Company of India (LIC), and covered 3.6 mln households as of 2006. In addition to the survivor benefit in case of death, JBY provides for Rs. 50,000 to a household in case of permanent total disability and Rs. 25,000 in case of permanent partial disability. This is based on an annual premium of Rs. 200 per household, half of which comes from the insured person and half from a Social Security Fund of LIC itself which was financed by GoI on a corpus basis. The program is targeted to group membership (of 20 and more members) and covers a designated range of unorganized sector occupations. The design of the scheme is interesting from a policy perspective in several ways. First, it is an attempt to incrementally increase coverage, in this case on the basis of occupations or groups considered to have generally lower incomes, but with some capacity to contribute. Second, there is a transparent subsidy intended to provide incentive for voluntary take up.

Welfare funds are most common in Southern India and in particular, Kerala where some estimates put coverage at more than one in five workers. In a recent review of Kerala welfare funds, Rajan (2002) found a wide variety of benefits including for very specific health conditions (e.g., artificial organs) to cash disability payments. Out of 24 welfare funds covered in the study, 18 offered some kind of disability benefit, but only 5 provided a monthly payment until death. The rest paid one time lump sum benefits. An ILO review of welfare funds in several states also found similar patterns.

The prevalence of disability benefits in micro-insurance schemes appears to be even more limited. In its review of 51 surveyed micro-insurance schemes, the ILO found that only one quarter offered disability benefits (although others did offer accident and health benefits that may overlap to some extent). The benefits were almost always in the form of lump sum payments. As an example, the Bharathi Integrated Rural Development Society (BIRDS), with about 9,000 contributors in 173 villages charges a premium for disability and life of 100 rupees per annum and pays a lump sum Rs. 25,000 in the case of permanent disability.

There is very little solid analysis available on how well these schemes function. Common challenges include relatively high administrative costs, limited risk pooling and lack of expertise in insurance. Moreover, given the general lack of regulation, there is bound to be wide dispersion in the quality and financial soundness of the different plans. Finally, even where the programs are functioning well, the public policy question is to what extent they can be scaled up.

Another source of disability coverage is the product offered by the New India Assurance Company (NIACL).

These publicly-owned companies are obliged to offer services targeted at specific groups. Coverage is extremely low however. For example, only 47,000 individual policies were sold for a disability insurance product targeted towards women offered by NIACL between 1998-2004. This is clearly a negligible fraction of potential coverage. Some of the rural insurance schemes with accident benefits appear to have greater coverage. It is unclear whether any of these products are priced on a fair basis or are implicitly subsidized by the insurance companies and ultimately by the state.

Separately, a bill had been introduced to Parliament that would introduce a New Pension Scheme (NPS) that would be available to any individual not already obligated to participate in schemes under the EPFO Act. The NPS was originally aimed at the informal sector but recently the central government and 15 state governments have determined that new government employees should enter the defined contribution scheme. Thus, when the NPS goes into effect, it will theoretically provide a platform for pension provision that would extend to both civil servants and informal sector workers.

By the end of 2005, an estimated 200,000 public sector workers were contributing ten per cent of their wages to their individual retirement account. This was being matched by the government as the employer. When the NPS infrastructure and regulations are finalized, these funds would be invested through professional asset managers through the capital markets. The accumulations over the course of the career would be partly annuitized at the point of retirement, replacing the current, non-contributory defined benefit pension scheme inherited from the colonial era.

Notably, the NPS has yet to define a disability or survivors benefit. This will be necessary at some point since these benefits were part of the old package for civil servants and new cases will be observed even during the first months of the scheme. In a defined contribution scheme, the risk of death or disability must be handled as an additional insurance policy and priced separately.

In principle, adding a group insurance policy for death and disability to a DC scheme of this kind is relatively simple. In Latin America for example, several countries insure the difference between the balance that is accumulated at the moment that the contingency occurs and the amount needed to purchase an annuity at a predetermined level on market terms. The premium charged for this year to year insurance policy is a function of the disability/mortality rate, the size of the contribution, contribution density16, the investment return and the level of the prescribed benefit.

Tying the insured amount to the individual account balance reduces the required premium relative to a stand-alone product. Gruschka and Demarco calculate that under reasonable assumptions for the parameters mentioned above - including a ten per cent contribution rate to the DC account - a replacement rate of 50 per cent could be financed for around 1 per cent of covered wages. The premium may be even lower in the case of Indian civil servants due to low disability rates, a higher contribution density and higher contribution rates (double those in the example).

While the design of the insurance package is straightforward, a number of practical challenges exist in implementation. First, in India and in most developing countries, relevant mortality statistics are not readily available, at least initially. This could be remedied over time through data collection and actuarial studies. Second, the private insurance market is still at an early stage in development and does not have experience in offering annuity products. Moreover, any attempt to include an indexed annuity would be complicated by the dearth of assets that could be used to hedge such a product. Nevertheless, these obstacles are surmountable as has been demonstrated by actual experience in Latin America.

Could such an approach be used to reach workers in the informal sector? In principle, the answer would seem to be ‘yes’, but again, the challenges lie in the implementation and especially the feasibility of controlling moral hazard and adverse selection. Encouraging informal sector workers to participate in a defined contribution pension scheme - a simple form of self insurance for old age - is straightforward and is already being implemented in India. One example is the unorganized sector provident scheme in West Bengal. In that particular case, the state government provides an incentive through a matching contribution of 20 rupees per month. After three years of operation, the scheme covers around 700,000 unorganized sector workers from a variety of occupations and the figure is rising.

While the DC scheme is the easiest to implement, most workers assign higher priority to short term benefits such as health, disability and life insurance. A survivors’ benefit is also relatively simple to design and to implement as a group insurance policy subject to the caveats raised earlier with regard to mortality tables and annuitization. Health insurance is clearly the most complicated if the coverage provided is to involve the service providers in any way.

The potential difficulties with disability insurance for the unorganized sector relate to the characteristics of this group of workers. Unlike civil servants where job security is high and workers are mandated to participate, many informal sector workers may experience bouts of unemployment or underemployment on a regular basis. They will also have information about their own risk profiles that may lead to adverse selection as those with safer occupations (rationally) opt out. Moral hazard opportunities are less likely as long as the insurance coverage was reserved for permanent and catastrophic types of impairments. Finally, the certification process to determine eligibility would be much more difficult to administer for this diffuse group of individuals, many of whom would be illiterate. This could provide opportunities for fraudulent medical certification or, on the other hand, demands for payments from applicants by doctors. Monitoring such a system would be a major challenge.

One way to address these concerns, at least in the first phase of implementation, would be to focus work primarily with existing groups, including some of those already mentioned. Larger groups that could ensure high rates of participation would be accorded highest priority. Another criterion would be agreement to abide by a standardized, uniform certification process. In addition to or instead of a direct matching contribution to the DC scheme, the state government concerned could simply pay for the survivors and disability insurance directly for the group. Again, it would be very useful to prepare the ground for such an initiative by closely tracking the mortality and disability rates of the members.

Recently GoI has developed proposals for expansion of social security to the unorganized sector which represent an alternative possible approach to expansion of disability insurance. The NCEUS proposal is ambitious in that it seeks to offer insurance for several major risks to 300 million informal sector workers in a span of five years. This includes disability insurance. The ultimate objective of universal coverage is shared by many developing country governments. However, such an expansion of coverage, to be achieved through voluntary participation is unprecedented in terms of international experience and experiences in India. The administrative and recordkeeping challenges alone suggest that the proposed time frame is not feasible.

In this vein, GOI (and specifically, MOLE and MOH) is in the process of building on the NCEUS approach towards a new policy that could be rolled out in stages. The first step in the sequenced expansion policy can be seen in the 2007-08 budget announcement of the Aam Aaadmi Bima Yogana (AABY). This is intended to cover around 15 million rural landless households with death and disability insurance for the breadwinner, with the premium fully subsidized on a 50/50 sharing basis by centre and states.

In time, the combined population of public sector workers, informal sector groups and some individuals could provide the volumes required for economies of scale of operation (say, in the tens of millions of contributors) and importantly therefore, consistent with low marginal costs of recordkeeping and fund management. The planned NPS scheme envisions this scale of operation and the information technology platform needed at a national level to implement it.19 Meanwhile, the commission to expand social security is tasked with producing a financially viable proposal to extend these kinds of benefits to unorganized sector workers. A convergence of the two initiatives would seem appropriate.

Recommendation

Policies and programs should help improve awareness and targeting of safety net benefits to the poor and develop innovative approaches to extend coverage of disability insurance.

Improving the safety net. A first step in improving the poor performance of safety net programs for disabled people is familiarizing implementing officials and PRI representatives of the commitments under the PWD Act. Once such familiarization is done, the next step is for implementers to make efforts to raise awareness of schemes and PWD entitlements. In parallel, efforts need to be made in the public and non-governmental sectors to mobilize PWD themselves, so that there is more bottom-up demand on the delivery system. Formation and capacity building of PWD SHGs could be an important part of both strategies. Developing more focused efforts are also needed for specific programs, including: (i) for SGSY, targeted efforts to mobilize formation of SHGs of disabled people; (ii) for NREGS, adjustment of the national guidelines to include disabled people and efforts to identify both categories of works well suited to disabled people and processes for ensuring their adequate inclusion; and (iii) for social pensions, review of states with poor coverage, and relaxing the eligibility criteria for disability social pensions. It would also seem sensible to consider a base level of funding from the central government on disability social pensions, just as happens presently with the NOAPS scheme for destitute old age people. The transfer under NOAPS was increased to Rs. 200 in the 2006-07 budget, and equity considerations suggest that disabled social pensioners should be treated on a similar footing. The experience of NOAPS with much higher beneficiary numbers suggests that this would be a highly affordable initiative in fiscal terms.

Expanding disability insurance. In order to address the demand that clearly exists for disability insurance, a low cost platform with standardized products and uniform regulations is likely to be the only approach that can be scaled up at the national level. Such a platform has recently been proposed under the New Pension System to deal with old age pensions for both the informal sector workers and civil servants. However, it will be necessary to have far more coordinated efforts across different arms and levels of government to link various social insurance initiatives to such a platform. Equally, the role of intermediary organizations such as MFIs, NGOs, and perhaps PRIs will be critical in improving program outreach and playing a role in contribution mobilization and claims processing if transactions costs are to be kept manageable.